Gartner believes that blockchain is set to produce $3.1 trillion in new company value by 2030. With the technology not expected to be ready for widespread implementation until later in 2023, companies should start investigating it right now.

Huge multinational firms and digital behemoths adopt blockchain components to increase their market dominance. Companies that manage to build a framework for implementing this technology are likely to compete more successfully in their markets.

As a result, leaders in small and mid-sized companies are under pressure to guide choices about whether and how blockchain may be used in their organizations. They need to grasp what blockchain is and how it can be used to advance mission-critical business goals—or even fundamentally disrupt the organization.

Blockchain introduces a host of challenges ranging from strategic issues such as how to compete while collaborating, lack of technical interoperability, security risks, and various data management and regulatory scenarios, including discussing different security and privacy laws such as the EU’s Global Data Protection Regulation (GDPR).

Read on to learn everything you need to know about blockchain as you step into 2023.

A blockchain is a distributed database or ledger shared across computer network nodes. Like a database, it saves data electronically in a digital format. What’s new about blockchain? It ensures the security of a data record and builds trust without having to use a trusted third party.

Blockchains are recognized for their critical role in cryptocurrency systems like Bitcoin, where they keep a secure and decentralized record of transactions.

Another difference between a traditional database and a blockchain lies in how they organize data. A blockchain accumulates information in blocks storing datasets. When a block’s storage capacity is reached, it is closed and connected to the previous full block, producing a data chain called a blockchain. All new information that follows that newly added block is assembled into another block added to the chain once it is complete.

A database typically organizes its data into tables, but a blockchain, as the name suggests, organizes its data into chunks (blocks) that are linked together. When implemented in a decentralized way, this data structure creates an irreversible data timeline. A completed block becomes permanent and forms a part of this timeline. Every block added to the chain gets a timestamp assigned to it.

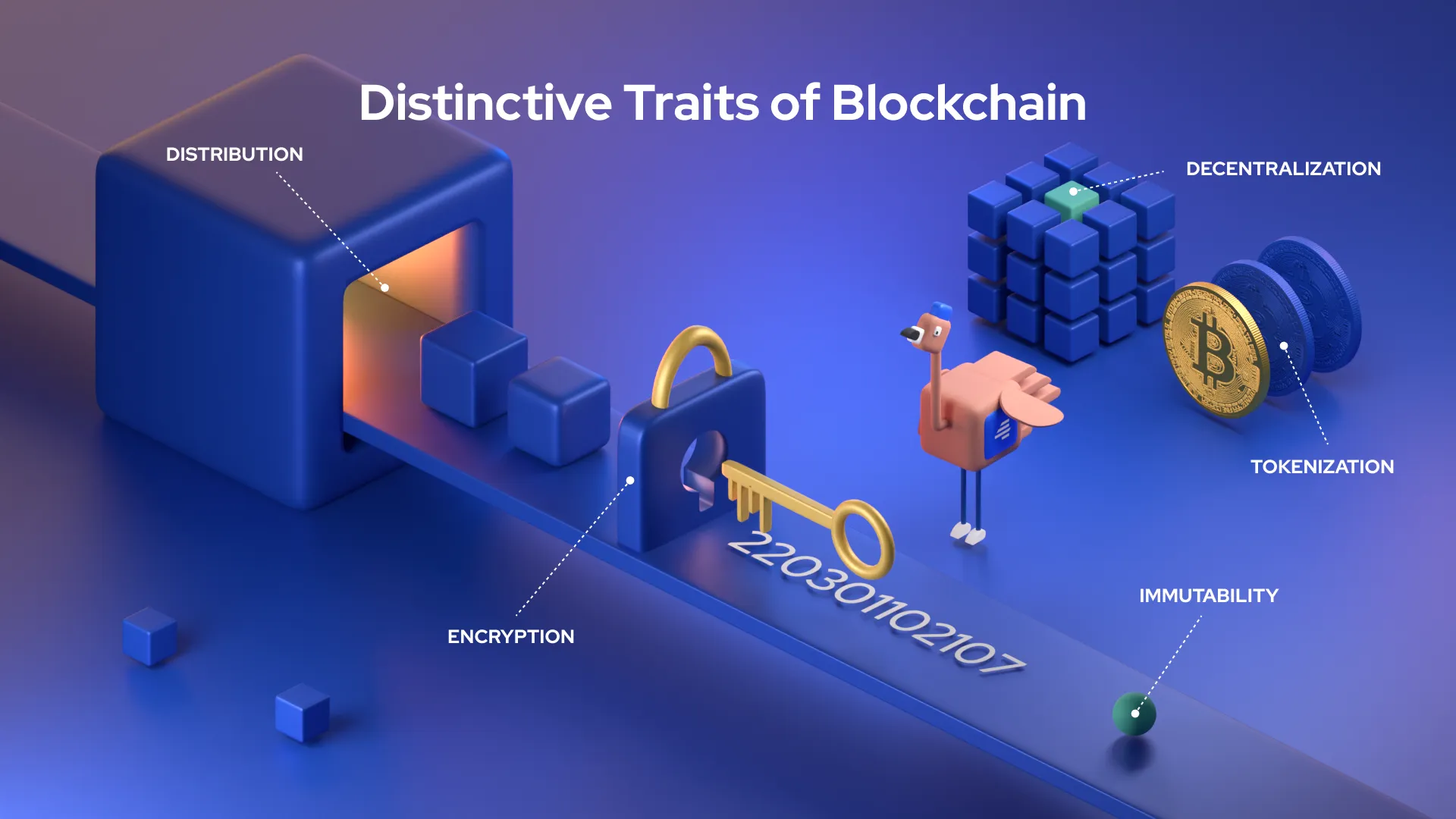

Distribution – blockchain members are physically separated from one another but linked via a network. Each participant running a full node has a complete copy of a ledger that is updated when new transactions occur.

Encryption – blockchain employs technologies such as public and private keys to securely and semi-anonymously record data in blocks (participants have pseudonyms). Participants may manage their identity and other personal information, and only reveal what is required in a transaction.

Immutability – transactions are cryptographically signed, time-stamped, and added to the ledger consecutively. Records cannot be corrupted or otherwise altered unless all parties agree to it.

Tokenization – in a blockchain, value is represented by tokens, which may be anything from financial assets to data to physical goods. Tokens also give members ownership over their personal data, which is a key driver of blockchain’s business case.

Decentralization – due to a consensus process, nodes in the dispersed network preserve both network information and rules. In practice, decentralization implies that no single entity controls all computers, information, or regulations.

Blockchain made its public debut with Bitcoin in 2009, when Satoshi Nakamoto published a whitepaper describing the idea.

However, the foundations of blockchain technology can be traced back to 1991, when physicist Stuart Haber and cryptographer W. Scott Stornetta presented a research paper entitled “How to time-stamp a digital document.”

The study explored the immutability of digital records using a Time Stamping Service (TSS), which combines hash functions and digital signatures to certify the authenticity of a document. The documents are then linked together to create a time sequence to validate the time stamps associated with each.

The simplest form of blockchain was a chain of papers with a time sequence, subsequently employed by Nick Szabo in 1998 to create Bit Gold, an early prototype of the digital currency. Still, Szabo wasn’t convinced about the execution of his concept.

Satoshi Nakamoto’s proposal in 2009 decoupled the value of Bitcoin from the cost of computing and let the value be established by the free market.

If the value is closely associated with the computing cost, it might produce inconsistencies in the network. One coin will become more valuable than the other due to the underlying processing cost. If the value of Bitcoin was associated with the cost of computation, then all Bitcoins mined in 2010 would be far cheaper than those created now, because the computing power required to mine a Bitcoin in 2010 was much lower.

Blockchain protocols are rules that enable data to be transferred across a network. They’re a collection of standards that make information sharing easy, efficient, and secure.

Protocols serve a crucial function in monitoring and securing a computer network. Since blockchains are used for transactions, protocols play a key role in data sharing to ensure the security of cryptocurrency networks.

A blockchain protocol is a collection of rules that govern the blockchain network. The rules determine the network interface, computer interaction, incentives, data type, etc.

Protocol sensure the safety of the whole crypto network. As the network involves the movement of money, protocols govern the structure of data while also protecting it from malicious users. When a transaction happens, protocols update the whole database at each step.

Scalability was formerly a concern in the blockchain space. However, most protocols today can deal with the rising number of transactions in the network.

No sector will gain more from implementing blockchain in its business processes than financial services. Banks are only open during business hours, usually five days a week. If you try to deposit a check on Friday at 6 pm, you’ll likely have to wait until Monday morning for the funds to appear in your account. And even if you make a deposit during business hours, it may take one to three days for the transaction to be verified due to the massive volume of transactions an average bank must settle.

By incorporating blockchain into banks, users can expect their transactions to be processed in as little as 10 minutes. It’s basically the time it takes to add a block to the blockchain, regardless of holidays or time of day.

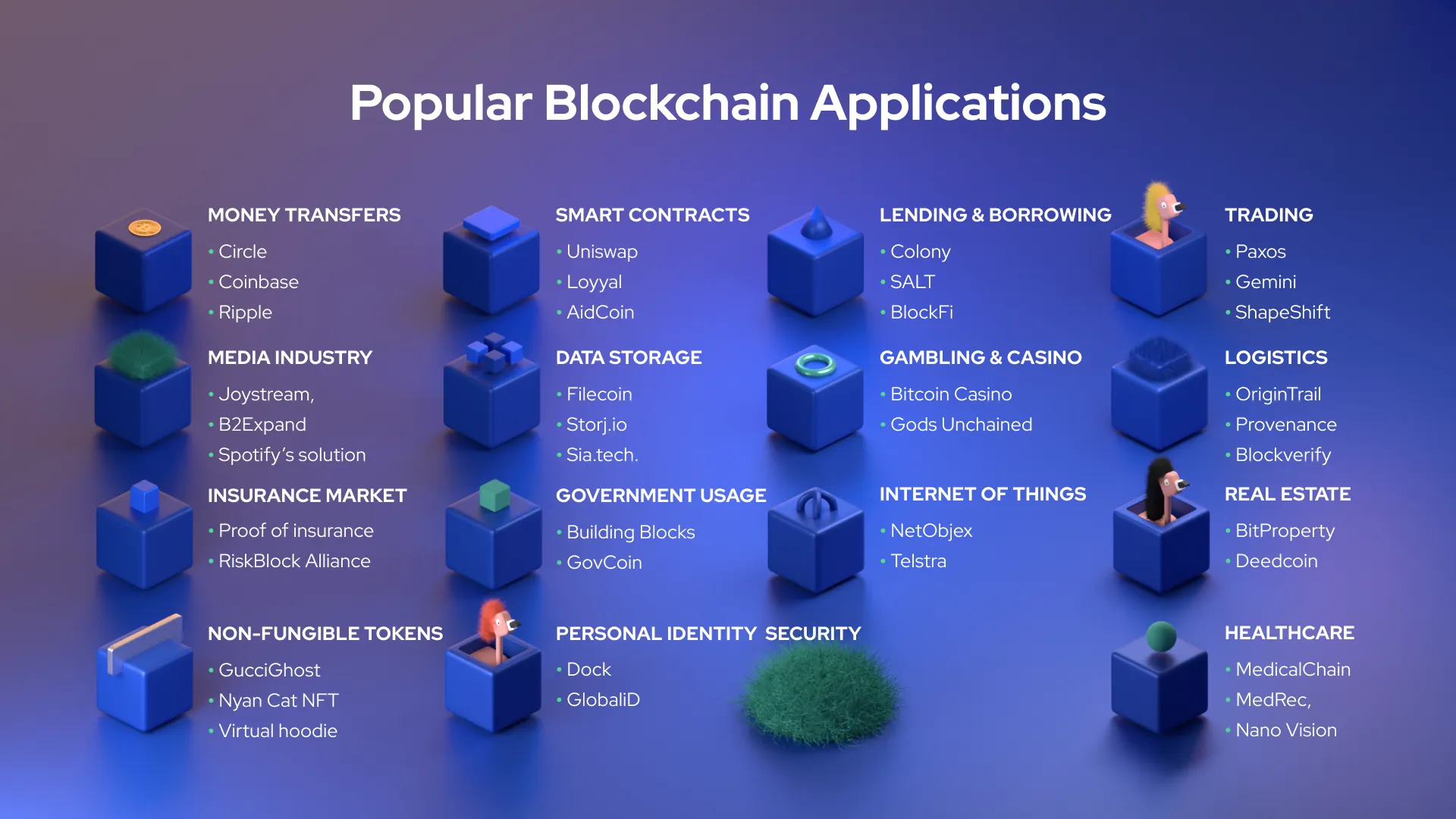

Example applications include:

Circle – the app lets users send money through text without any fees.

Coinbase – one of the largest exchanges that allows users to buy, sell and store over 150 cryptocurrencies and convert them into fiat currency.

Ripple – this app helps users send money and make payments via 175+ banks and commercial platforms.

In the stock trading industry, the settlement and clearing procedure can take up to three days (or more if dealing overseas), which means that the funds and shares are frozen during that time.

Given the magnitude of the funds involved, even a few days in transit might incur enormous expenses and hazards for institutions. Banks may also use blockchain to trade funds across institutions more swiftly and securely.

Example applications:

Paxos – using blockchain, this platform settles trades instantaneously, automates payment processes and eliminates third-parties.

Gemini – this app lets users buy, sell or store digital assets on its platform. The company created the world’s first government regulated stablecoin, Gemini Dollar (GUSD).

ShapeShift – the app facilitates real-time, secure cryptocurrency swaps using blockchain.

Lending providers can employ blockchain smart contracts to perform collateralized loans. Certain events, like a service payment, a margin call, the complete repayment of the loan, and collateral release, can be triggered automatically by smart contracts. This makes loan processing faster and more cost-effective, allowing lenders to offer lower interest rates.

Money transfers, lending, and trading are all part of the Decentralized Finance ecosystem. Its landscape is rapidly evolving thanks to platforms like Colony, a community-driven accelerator for DefI projects.

Other examples include SALT, which provides cash loans that use digital assets with an APR as low as o.52%, and BlockFi, a lending platform that uses crypto as collateral.

A smart contract is a piece of computer code that may be embedded in the blockchain to help facilitate, verify, or negotiate a contract agreement. Smart contracts operate under a set of agreed-upon conditions. When the requirements are satisfied, the provisions are implemented immediately.

Imagine a potential tenant who wants to rent an apartment using a smart contract. The landlord agrees to provide the renter with the apartment’s door code as soon as the tenant pays the security deposit.

Both the renter and the landlord would transmit their respective shares of the agreement to the smart contract, which would save the door code and immediately swap it for the security deposit on the lease start date. If the landlord fails to provide the door code by the lease expiration date, the smart contract returns the security deposit. This would help avoid the expenses and processes involved with using a notary, a third-party mediator, or attorneys.

Smart contracts need to be audited. If you place something into the production network, you won’t edit it too much (unless you’ve adjusted the product to allow it). Uniswap is a good example here.

Other interesting examples of smart contract-based applications include:

Loyyal – a loyalty and rewards platform that lets users create customized programs.

AidCoin – a platform that aims to improve people’s trust in charities using distributed ledgers, smart contracts, and cryptocurrencies.

Tracking components that travel on airplanes or vehicles is crucial for both safety and regulatory compliance. IoT data recorded in shared blockchain ledgers allows all stakeholders to track component origins throughout the life of a product.

Thanks to blockchain, sharing this information with regulatory bodies, shippers, and manufacturers is safe, simple, and cost-efficient.

IoT devices monitor the status of essential machinery and their maintenance. Blockchain steps in to provide a tamper-proof database of operating data and the resulting maintenance for everything from engines to elevators.

Third-party maintenance partners can keep an eye on the blockchain for preventative maintenance and log their activity on it. To ensure compliance, companies can share operational records with government bodies.

Here are two examples of applications that bring IoT and blockchain together:

NetObjex – a smart parking solution that helps drivers find a vacant space in the parking lot and automates payments using crypto-wallets.

Telstra – a telco and media company that offers smart home solutions using blockchain and biometric security.

Challenging identification paperwork processes, costs, a lack of access, and a general lack of understanding about personal identity are the key barriers that keep over a billion people outside of traditional identification systems. Without it, they can’t enroll in school, apply for jobs, obtain a passport, or access numerous government services.

Having an identity is key for gaining access to the current financial system as well. In contrast, 60% of the world’s 2.7 billion unbanked individuals currently hold mobile phones. The spread of technology paves the path for blockchain-based mobile identification solutions that suit the requirements of vulnerable individuals.

Examples of personal identity security companies that use blockchain:

Dock – a Verifiable Credentials company that offers a user-friendly, no-code platform to help companies issue, manage and verify fraud-proof credentials.

GlobaliD – a platform that issues self-sovereign identities.

Healthcare providers may use blockchain to securely keep medical records for their patients or support doctor decision-making processes. When a medical record is created and signed, it can be stored on the blockchain to give patients proof and assurance that nobody can alter it.

These personal health records might be encoded and kept on the blockchain with a private key, making them available only to certain individuals and maintaining privacy. These are just a few of the many blockchain use cases in healthcare.

A good example is MedicalChain, a healthcare company that uses blockchain to facilitate the storage and utilization of electronic health records for telemedicine. Other examples are MedRec, which helps medical providers secure the access to patient records, and Nano Vision, which aims to break the traditional data silos and incompatible records systems to channel innovation.

Including blockchain in a data storage system boosts security and integrity. Data kept in a decentralized way is safer because hacking into the network is harder. A centralized data storage provider may suffer from vulnerabilities.

That way, blockchain also increases data availability because it doesn’t always depend on the activities of a single organization. Using blockchain for data storage may also be less expensive in some scenarios.

The open-source cloud storage marketplace, protocol, and incentive layer Filecoin is an example of blockchain storage use case. Other blockchain storage platforms are Storj.io and Sia.tech.

Suppliers may utilize blockchain technology to track the provenance of products they acquire. This would allow businesses to validate not only their own products but also popular labels like “Organic” or “Fair Trade.” The food sector can use blockchain to monitor the supply chain and safety of food along the farm-to-user journey.

An example of such an application is OriginTrail, a platform that shows consumers where their purchases came from and how they were produced. Other examples include Provenance, which brings transparency regarding the products consumers purchase and consume, and Blockverify, which focuses on anti-counterfeit solutions using blockchain to verify counterfeit products or fraudulent transactions.

Non-fungible tokens (NFTs) are blockchain-based tokens representing unique assets such as a work of art, digital property, or media. An NFT is an irreversible digital proof of ownership and authenticity for a specific item.

NFTs are intended to be cryptographically verifiable, unique or rare, and easily transferable among individuals. Using cryptographic signatures intrinsic to the blockchain on which an NFT is generated, you can determine the origin and current holder of the asset in question in seconds.

Examples of NFTs:

GucciGhost – created by artist Trevor Andrew who combined the Gucci logo with his graffiti art as part of the NFT collection called “Nifty Ghost Collection” which sold out in 12 seconds.

Nyan Cat NFT – based on the video meme that rose to prominence in 2011, sold for $600,000.

Virtual hoodie from Overpriced, a company that creates “fashion for the crypto generation,” sold for £19,000.

A strong trend in this space is fractional NFT that can be divided and distributed across many users. By lowering the entry barrier and enabling fractional ownership, fractionalized NFTs let average collectors to purchase high-value NFTs like luxury yachts and real estate.

The gambling sector can benefit from blockchain in a variety of ways. One of the biggest advantages of running a casino on the blockchain is the visibility it delivers to potential gamblers. They can quickly verify that the games are fair and the casino pays out since every transaction is logged on the blockchain and is fully transparent.

Furthermore, by using blockchain, no personal information is required to get started, which may remove a significant barrier for some would-be gamblers. It also circumvents regulatory constraints because participants may wager anonymously and the decentralized network is not vulnerable to government closure.

Examples include:

Bitcoin Casino – gambling platform with integrated cryptocurrencies that combines transaction speed with secure payments.

Gods Unchained – a collectible card game based on Ethereum for establishing cards ownership tracking.

Blockchain opens the door to a new type of voting system. Voting that uses blockchain has the potential to reduce election fraud while increasing voter turnout, as demonstrated in the November 2018 midterm elections in West Virginia.

Using the blockchain in this way would make tampering with votes next to impossible. The blockchain protocol also ensures transparency in the electoral process by lowering the number of people required to carry out an election and giving officials near-instant results. This would remove the need for recounts and any serious possibility of electoral fraud.

Other examples of blockchain applications in this area are Building Blocks, a UN World Food Program humanitarian platform that uses Ethereum, and GovCoin used to develop a blockchain for welfare payments.

The media industry faces increasing issues such as digital piracy, fraudulent copies, infringing studio intellectual property (IP), and digital item duplication. In the US, they cost the industry an estimated $71 billion each year. Blockchain can potentially change this,

For example, Enterprise Ethereum enables artists and producers to digitize the metadata of their original material and manage and maintain intellectual property rights on a time-stamped, immutable ledger. The blockchain’s append-only nature makes it easier for authors to legally assert their rights when an infringement happens.

A great example of a media company based on blockchain is Joystream, a video streaming platform that aims to achieve the state of autonomous governance. Other examples include B2Expand – a company that creates cross-gaming video games and Spotify’s solution for a decentralized database built with the blockchain startup Spotify acquired, Mediachain Labs.

Blockchain and insurance market

Blockchain fosters trust among insurers by offering a network with regulated access and a secure mechanism to transmit critical information. Insurers are still sluggish to embrace the technology, but we are seeing more and more firms build various proofs of concept and begin to exploit blockchain in various ways.

To date, the most notable use of blockchain has revolved around parametric triggers. If there is a flood or high wind, a smart contract might trigger a policy without any human intervention. If the customer matches all of the criteria, they might be compensated immediately via blockchain.

An interesting example of this use case is a product tested by Proof of insurance, a nationwide insurance company. The blockchain solution provides proof-of-insurance information called RiskBlock. Another company experimenting with blockchain is Nationwide Insurance, which joined the RiskBlock Alliance and its blockchain platform.

The process of documenting ownership rights is both time-consuming and inefficient. In the event of a property dispute, property claims need to be reconciled with the public index.

This method is also susceptible to human mistakes, with each inaccuracy making property ownership monitoring less efficient. Blockchain can remove the necessity for document scanning and physical file tracking at a local recording office, streamlining the process to make it much more efficient.

An example of this application is BitProperty that aims to democratize the opportunity to invest in real estate using blockchain. Another example is Deedcoin, a platform that helps connect home buyers and sellers with real estate agents.

Avalanche – a cryptocurrency and blockchain platform based on the Avalanche blockchain, which uses smart contracts supporting various blockchain projects.

Cardano – a proof-of-stake blockchain platform, the first one based on peer-reviewed research and developed using evidence-based methods.

Chainalysis KYT – this platform brings together industry-leading blockchain intelligence, a real-time API, and a sleek interface to help companies reduce manual workflows, and stay compliant while working with blockchain products.

Ethereum – a decentralized, open-source blockchain that has smart contract functionality, with Ether as its native cryptocurrency, which users can keep in blockchain wallets.

Hyperledger Fabric – an open-source blockchain framework hosted by The Linux Foundation with a vibrant community of developers.

Hyperledger Sawtooth – an open-source enterprise blockchain-as-a-service platform for running customized smart contracts, operated by an umbrella blockchain development group sponsored by the Linux Project, IBM, Intel, and SAP.

IBM Blockchain – IBM’s commercial distribution of Hyperledger Fabric, including full support with SLAs and a set of advanced productivity tools.

Polkadot – a blockchain platform and cryptocurrency (DOT), designed to let blockchains exchange messages and carry out transactions without a trusted third party.

Ripple – a real-time gross settlement platform that also works as a currency exchange and remittance network.

Solana – an open-source blockchain platform for hosting decentralized and scalable applications.

Tezos – an open-source platform that solves key barriers around blockchain adoption for assets and applications, backed by a worldwide community of validators.

Tron DAO – a protocol that aims to accelerate decentralization, empowering developers and putting the power back in the hands of the community.

XDC Network – a hybrid blockchain based on a delegated proof-of-stake (XDPoS) consensus mechanism.

Quorum – an open-source, permissioned blockchain protocol based on Ethereum developed by J.P. Morgan.

Stellar – an open-source, decentralized protocol for low-cost transfers of digital currency to fiat money.

A blockchain network is a type of technological infrastructure that allows apps to connect to the ledger and smart contract services. Smart contracts are used to initiate transactions, which are then sent to each peer node in the network and immutably recorded on their copy of the ledger.

App users include end-users who use client applications and blockchain network administrators. A blockchain network can monitor orders, accounts, payments, production, and much more. Since members share a single version of the truth, they can see all the facts of a transaction from beginning to end.

A public blockchain is one everyone may watch, submit transactions to, and expect those transactions to be included if genuine. It also allows everyone to participate in the consensus process, which selects which blocks are added to the chain and what the current state is.

Cryptoeconomics protects public blockchains by combining economic incentives with cryptographic verification methods such as proof-of-work (Bitcoin) or proof-of-stake (Ethereum). These blockchains are considered fully decentralized.

Hybrid blockchains combine the fundamental components of both public and private blockchains to secure transactions and data. Examples include the Aergo Enterprise-Samsung hybrid blockchain system or Swisscoin, a new cryptocurrency that operates on a hybrid blockchain.

Private blockchains are permissioned blockchains operated by a single entity. Private blockchains include Ripple, a business-to-business virtual currency exchange network, and Hyperledger, an overarching project for open-source blockchain applications.

Consensus algorithms

Blockchains work by adding blocks of data, and the goal of consensus is to make sure that every block added to the chain represents the sole version of reality that all system nodes have agreed upon. It is a crucial aspect of blockchain’s decentralized structure. Blockchain algorithms come in various shapes and sizes:

Proof of Work (PoW)

“Classic mining” refers to the Proof of Work consensus algorithm used in Bitcoin and Ethereum. The block validator is a cryptographic problem solved with brute force (and a little bit of probability). In essence, it acts as a fence to prevent attacks on the blockchain. You must produce equivalent power if you wish to use the blockchain for any purpose.

Proof of Stake (PoS)

This second-most common consensus algorithm is more efficient. Miners can verify their engagement by betting part of their tokens on the new block. A pure PoS solution has no incentive to vote fairly on forks because of the “nothing at risk” dilemma. This may lower ledger credibility.

Proof-of-Authority (PoA)

In this blockchain algorithm, admins validate transactions in this centralized solution. Proof-of-Authority consensus is scalable and fast for private networks. It removes one of blockchain’s main benefits, yet it may work for other businesses.

Proof-of-Weight (PoWeight)

Proof-of-Weight sets your block-mining probability. You can specify any quantity connected to the node, such as the amount of blockchain data on your drive, or any other unique weight.

Byzantine Fault Tolerance (BFT)

Byzantine Fault Tolerance solves a classic problem—generals contemplating an assault on a besieged city. They must decide to attack or break the siege. Some generals may be traitors and vote to retreat. Ripple and Hyperledger leverage this low-cost, scalable method.

Blockchain will remain at the forefront for the next few years as organizations and startups will keep developing services that can combine blockchain apps with non-blockchain data, as well as services that operate on incompatible blockchains, prioritizing scalability and security.

Blockchain technology is on its way to maturing into a robust platform for the apps and services we all want, powered by innovations in fields such as blockchain governance or compliance, inspiring startups like Elliptic to create unique solutions for the blockchain world.

Do you want to become part of the exciting blockchain scene?

We can help you build your project and set it up for success thanks to our deep understanding of the latest technologies gained during 9+ years of developing blockchain applications. We provide customized solutions for increased efficiency, security, and transparency in operations. Check out our success stories on this blockchain development page.